NONPROFIT YEAR-END FINANCIAL STATEMENT AUDIT (OR REVIEW) PROCESS IN A NUTSHELL (PART 4 of 5)

THE YEAR-END FINANCIAL STATEMENT PROCESS:

A Practical Guide for Small Nonprofit Organizations having a CPA Audit (or Review)

(Part 4 of 5)

Part IV: Preparing for the Annual Audit (or Review)

A. Financial Data: Are your books ready for the audit (or review)?

In many cases, smaller, volunteer run, nonprofit organizations have a good grasp of their finances. In some cases, they are even better than larger organizations. Smaller organizations have few complex transactions and often the governing board and management are familiar with all aspects of the organization. A careful review at year-end can enable the organization to identify any potential adjustments needed for the financial data. Most organizations, through internal staff or an external accountant/bookkeeper, can post these adjustments in the accounting system. Other organizations may present the information to the auditor. The auditor can enter adjustments and, under the right conditions, propose accounting adjustments. Keep in mind, the accountant cannot make major overhauls of financial data while performing an attest engagement. A QuickBooks file could be sufficient to present the financial statement data to the accountant.

Since the organization’s trial balance shows accounts at the most detailed level, each line in the trial balance should be reviewed. The organization needs to understand and be able to explain what amounts comprise each account. Comparing the balances to the prior year can help to identify any possible adjustments. Smaller organizations tend to concentrate on profit and loss accounts (revenues and expenses) throughout the year with a focus on how they compare to budgeted amounts. Balance sheet accounts are often given less attention. Balance sheet accounts represent accounts that have a measureable value at the year-end date, including all assets and liabilities. An auditor will need to verify almost every item on the balance sheet. Organizations should pay careful attention to balance sheet accounts that are unadjusted from the prior year or have items posted to them inadvertently. While looking at the trial balance, organizations should consider reviewing their chart of accounts. An orderly chart of accounts can also help the year-end audit or review process. All journal entries, especially year-end or non-reoccurring entries, should be reviewed. The auditor will analyze these entries and ask for supporting documentation, if necessary.

Size of an organization, materiality and other factors dictate the level of preparation needed for a particular account. Below are some specific accounts with examples on how a small nonprofit could prepare these areas for year-end process.

· Bank Accounts: Bank accounts should be reconciled in QuickBooks (or manually). Review the bank reconciliation (or the bank reconciliation report from QuickBooks). Specifically (a) Make sure the register (book) balance from the reconciliation ties out to the trial balance (or balance sheet) amount (b) make sure the cleared (bank) balance ties out to the bank statement, and (c) make sure all uncleared checks and deposits are valid, void any checks or deposits, as necessary.

· PayPal: Treat PayPal like a bank account. PayPal should have a separate account (i.e., in QuickBooks). All original transactions should be posted to the PayPal account (e.g, deposits, PayPal fees, and debit transactions). Amounts going from the PayPal account to a bank account should be booked as transfers (as would be done when transferring amounts between any bank accounts.) Many PayPal accounts have a zero balance since they are set to automatically transfer to a checking account. Other PayPal accounts maintain a balance. The PayPal account should be reconciled to the year-end statement similar to the bank account reconciliations.

· Credit Card Accounts: Each credit card account should have a separate account in QuickBooks. All transactions should be posted to the account. This account could be reconciled to the year-end statement similar to the bank account reconciliations.

· Line of Credit Accounts: All lines of credit need a separate quickbooks account. These accounts should also be reconciled to the year-end statement similar to the bank account reconciliations. The auditor will need the terms and maturity date of the line of credit.

· Investment Activity: The auditor will need to be able to separate all the elements of the investment activity (Interest, Capital Gains, Dividends, Realized Gains, Realized Losses, Unrealized Gains, Unrealized Losses). We will also need a breakdown of the investments by Type (US Stocks, Corporate bonds, Government bonds). If you have a simple investment portfolio most of this could be derived from the year end statement and annual reports. More complex, active portfolios will need additional information.

· Fixed Assets: The auditor will need a list of property and equipment. This should show the prior year amount, additions, disposals and depreciation expense for the year. It is possible this information is contained in the company’s QuickBooks file. Please review the capitalization policy. This sets the amount in which one would expense an item rather than capitalize/depreciate. A capitalization policy of $2,000 or higher is recommneded. If there are smaller purchases, it may be proper to book to office expense or another expense item. A depreciation entry for the year will need to be booked.

· Payroll: Payroll should be reported at gross amounts. If this is not done through periodic entries throughout the year, a journal entry would have to be made to gross it up at year end. The final income statement (aka statement of activities) should have separate amounts for gross payroll, payroll tax expense, retirement benefits and health insurance. On the balance sheet (aka statement of financial position) you should show any payroll tax liabilities (payroll taxes for current year payroll that are paid in the following year), and accrued payroll (to account for payroll periods that cross the year end date). The auditor will also need to separate the amount of payroll, retirement benefit expense and health insurance expense allocable to the executive director.

· Accrued Vacation or Time off: Please review the company’s personnel manual. If employees are able to carry over days, whether to be used in the future or paid out, there should be a liability reflected for this amount on the balance sheet. Most organizations calculate this on an excel schedule by employee. Policies have to be read carefully. If amounts are not payable upon termination or could expire, then a decision has to be made on the amount to record as a liability.

· Accrued Expenses: Amounts owed at year end need to be accounted for. Check items such as consultants, professional fees and rent. Payments can be reviewed at the beginning of the following year to see if the services were performed in the audit period. Adjust amounts that are material to Accrued Expenses (other current liability account).

· Prepaid Expenses: Amounts prepaid at year-end need to be accounted for. Check items such as rent, insurance, and advertising. Adjust amounts that are material to Prepaid expenses (other current asset account).

· Deferred Revenue: If a program service revenue driven organization (paid of services, not supported by contributions), the company may need to track revenue paid in advance. Schools that received tuition in advance and performance organizations that received payments in advance, would be examples of this. The CPA would need the amount that was already received at year-end for services to be performed in the subsequent year. This would go to a liability account called “Deferred Revenue” This does not apply to Contributions (gifts, grants etc.). Contributions received, that are to be used in a future period because of a donor stipulation, would be restricted assets. See “restricted assets”

· Cost Reimbursement Contracts: Grants received by the organization are evaluated on an individual basis, based on grant specifications, to determine appropriate recognition as either a contribution or cost reimbursement grant. Grants determined to be contributions are recognized as revenue in the year awarded. For grants determined to be cost reimbursement awards, grant revenue is recognized as costs are incurred. Funds received in excess of costs incurred are recorded in a liability account (e.g., deferred revenue or refundable advances)

· Restricted Assets: A unique item in nonprofit accounting is the treatment of restricted assets. If a donation, grant or other contribution is made, and the donor specifically restricts the funds to a certain use, it has to be tracked. This would also apply if fundraising is for a specific cause (e.g., to build a youth center or to help with a specific natural disaster). Donations made to help the organization fulfill its general mission, are not restricted. For restricted donations, a running balance should be kept on amounts received, amount used for that restricted purpose and amounts remaining to be spent. There are ways QuickBooks can help track this, but it is not an integrated feature. This can normally be done using the QuickBooks data and an excel worksheet. Restricted funds received are booked as normal income items (i.e., Contributions or Grant income). The income is not “deferred” it is just “tracked.”

· Special Events: Special Events (aka fundraisers) need to be accounted for carefully. Normally, special events income and expenses are both accounted for in the income section. This is the presentation on Form 990. Most financial statements are formatted this way, as well. Having a good chart of accounts is helpful to booking special events correctly (see sample Chart of Accounts). If contributions are combined with exchange transactions, it needs to be broken out. For example, a ticket to a fundraiser dinner would include an exchange portion (what you pay for the dinner) and a contribution portion (what you pay above the value of the dinner). This breakout should correspond to the acknowledgement letter given to the donors. For auctions many details have to be tracked separately, as well.

· Functional Expense Allocations: Nonprofits, similar to other types of organizations, need to sort expenses by their “Natural” classifications. A natural classification would be normal expense accounts such as payroll, rent, office expense, insurance etc. In addition to this, nonprofits need to allocate their expenses by function. In the simplest form, this would be to also allocate the expenses by Program, Administration and Fundraising. Many smaller nonprofits have one program, but if an organization has multiple distinct, material programs, it should be allocated among the programs as well (i.e., Program 1, Program 2). Form 990, Part IX, statement of functional expenses, shows the functional expense allocation. An organization needs to identify expense lines that are 100% in a functional category and also expenses that are allocated. For example, a program director may be 100% program expense, but an executive director or rent may be allocated over several functional categories. This can be done in QuickBooks using “class tracking”. Organizations can also show the functional expense allocation by preparing a memo specifying the percentages for accounts to be allocated or show allocation percentages by account on an excel sheet.

· Noncash Contributions: Transactions not involving cash are prone to be left unrecorded. Due to the nature of Nonprofits, this is frequently a significant item. Noncash contributions have to be recorded as income. Noncash items distributed have to be reported as an expense. For example, a food pantry that receives food donations and then distributes the food would record Income (Noncash contribution – Food) and an expense (Food – Distributed). If there is food remaining on hand, there would be a food inventory account. Other material noncash items received need to be reported as well (e.g,. cars, supplies, furniture, real estate, stocks, and auction items). Noncash contributions are recorded on the financial statements (GAAP) and on the form 990. Form 990 also has a schedule M where one would need further detail on Noncash transactions.

· In-kind Contributions: In-kind contributions are different from Noncash items. In-kind contributions are donations of services or use of facilities. This is an item recorded for the financial statements (GAAP) but not on form 990. Form 990 – Schedule D has a schedule in which one can reconcile the GAAP financial statement to the Form 990. In-kind Contributions would be a reconciling item. In-kind services that need to be recorded are typically professional fees such as Pro-bono Lawyers, accountants or other professionals. Regular “volunteers” are not recorded. Look up the specific rules on this if there is a question. In-kind Facilities (i.e. free rent) and Advertising (free ad space or commercials) also have to be recorded. All of these items need to be valued at the fair market value the organization would have paid if they were not provided in-kind.

B. Governance Items Needed for the year-end audit (or review)

The year-end process, especially in the case of an audit, will focus on governance. Below is a list of governance items the organization may be expected to provide.

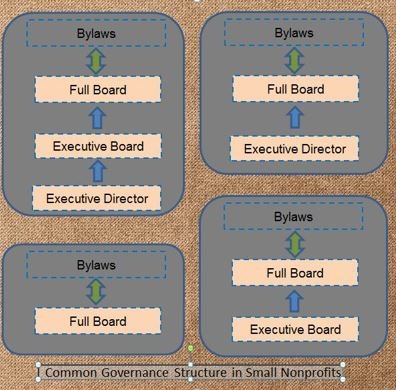

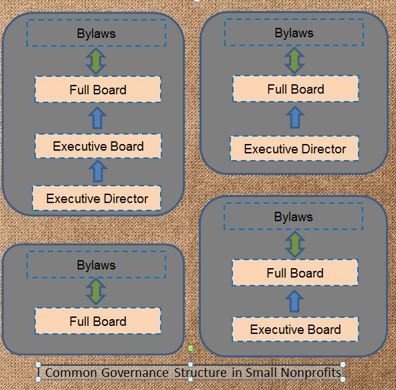

· Bylaws: An organization should be intimately familiar with their bylaws as it sets out the rules in which the organization will operate. A copy of the current bylaws should be readily available.

· Board of Directors’ Minutes: All Board of Directors’ Minutes from the beginning of the fiscal year to the most current meeting should be made available. This would include executive committee, finance committee and audit committee meetings.

· Conflicts of Interest Policy: The conflicts of interest policy is of upmost importance to a nonprofit organization. Organizations are assumed to have a current conflicts of interest policy with a requirement for Annual Statement in order to meet minimum good governance standards recommended by the IRS. A conflict of interest policy is also mandated in many states.

· Formation and registration documents: Articles of Incorporation, IRS Form 1023, State Charity registration form and state sales tax exemption forms should be available

· Other Policies and Procedures: The CPA will ask for major policies and procedures such as a Whistle Blower Policy, Record Retention and Document Destruction, Executive Compensation Policy, Form 990 and Audit review policy Employee/personnel manual, gift acceptance, and Investment Policies.

· Accounting Policies and Procedures Manual: Process (i.e., Cash disbursements, approval process, processing payroll, making deposits, accepting gifts or grants, petty cash, etc.)

· Employee or Personnel Handbook: Any written documentation concerning vacation and sick time, Accrued vacation policy, health insurance coverage, other benefits will need to be reviewed by the CPA

C. Other Items Needed for the year-end audit (or review)

In an audit, the CPA is required to obtain an understanding of the business’s internal control and assess fraud risk. The CPA is also required to corroborate the amounts and disclosures included in the financial statements by obtaining audit evidence through inquiry, physical inspection, observation, third-party confirmations, examination, analytical procedures and other procedures. The following is a list of items that may be requested in an Audit (or review) engagement.

□ Bank statements

□ Bank reconciliation reports (explanations for any outstanding checks still not currently cleared)

□ Credit card statements

□ Line of credit statements

□ Quarterly payroll tax returns (IRS Form 941 and state forms)

□ Annual payroll tax forms (forms W2/W3 and 1099/1096)

□ Grant contracts

□ Letter or correspondence that accompanied any large donations

□ Information on any audits by funders

□ Information on any fraud

□ The work of attorneys or any legal proceedings (paid or pro-bono)

□ Noncash contributions and in-kind services

□ Copies of current leases

□ Loan agreements

□ Information about related party transactions

□ Examinations from the IRS or State

□ Invoices for services billed

□ Bills and other receipts for expenses

□ Special events details (including auctions)

□ Inventory count workpapers

□ Schedule of Accounts Receivable (explanations of any amounts not received since the year end date)

□ Schedule of accounts payable (explanations of any amounts not paid since the year end date)

□ Property additions, deletions and depreciation schedule

□ Functional expense allocations

□ Temporarily restricted net assets (additional amounts and amounts released)

□ Copies of Donor Acknowledgment letters

Form 990 and other annual filing requirements

Form 990: Tax exempt organizations are required to file some version of Form 990 annually (some exceptions apply, for example, certain religious organizations)

State filings: States have varying filing requirements. Many states require a copy of the IRS Form 990 to be filed with the state. Some require an organization to attach audited or reviewed financials. Each state has different registration requirements for charitable organizations. Whether an organization has to register in a given state (and file annually) depends on that state’s regulations and the organization’s activities in that state.

NONPROFIT YEAR-END FINANCIAL STATEMENT AUDIT (OR REVIEW) PROCESS IN A NUTSHELL (PART 3 of 5)

THE YEAR-END FINANCIAL STATEMENT PROCESS:

A Practical Guide for Small Nonprofit Organizations having a CPA Audit (or Review)

(Part 3 of 5)

Part III: Deliverables and Outputs of the Audit Process

A. Financial Statements and Audit Report

At the end of the engagement, the auditor will present the organization’s financial statements and footnote disclosures into a generally accepted format. The financial statements will be preceded by the Auditors Report. This report will state whether the financial statements are “presented fairly, in all material respects.” It is this “assurance” that enables the users of the financial statements to rely on them. Almost every audit will have an “unqualified opinion”, which is the best outcome. The reason for this is that any adjustments the auditor “proposes” will most likely be accepted and posted by the organization. A “qualified” opinion would be an “except for” opinion. It means the auditor agrees with the financial statements except for a particular item. The last opinion is an “adverse” opinion. That would mean the auditor is stating the financial statements are “not presented fairly”.

B. Auditor Communications

Besides the Auditor’s Report on the financial statements, there are other items the auditor will report to the organization. These auditor communications can be broken into three areas: (1) required communications to governance; (2) a report on internal control deficiencies; and (3) recommendations for strengthening internal controls and operating efficiency. The ways auditors communicate these items to the organization varies.

(1) Required Communications to Governance: This is usually in letter form and will highlight to governance key aspects of the audit and the financial statements. This will include complex accounting policies, significant estimates, important disclosures (footnotes), difficulties encountered in performing the audit, and disagreements with management. Also, there would be information about uncorrected and corrected misstatements. Corrected misstatements would be the adjustment entries that were proposed and accepted. There would normally not be any material uncorrected misstatements in a small nonprofit audit.

(2) Internal control deficiencies: Although it is not the purpose of the audit to render an opinion on internal controls, the auditor is required to report any significant deficiencies in internal control encountered during the audit.

Generally Accepted Auditing Standards advise that a deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency or a combination of deficiencies in internal control, such that there is a reasonable possibility that a material misstatement of the organization’s financial statements will not be prevented, or detected and corrected, on a timely basis.

Since almost all organizations receive an unqualified opinion on the financial statement audit report, the internal control communication letter could be the most important output of the audit. It is common for a small nonprofit audit to result in some significant deficiency findings. Correcting internal control deficiencies is critically important to the financial health of all nonprofit organizations. Weaknesses in internal control can impact financial reporting or entice someone to perpetrate fraud. Common deficiency findings in nonprofit audits involve segregation of duties, oversight of financial reporting, monthly reconciliation and closing procedures, controls over cash and governance issues. The items identified in the internal control letter should be reviewed and addressed by the board and management. Many organizations develop a written response and action plan for each item.

(3) Recommendations: During the audit process the auditor may become aware of opportunities for strengthening controls and operating efficiency. These may be internal control items not deemed material enough to be included in the internal control letter. These also may be items involving issues that are not directly related to the audit such as Form 990, payroll filings, other general business items. If not addressed, items on the recommendation letter may escalate to deficiencies in future periods. The “recommendations” should be reviewed and addressed by the board and management, as well. These recommendation items are not required by auditing standards and can be communicated orally during the course of the audit.

Although written communication letters are addressed to the organization, they are often requested by outside parties, such as funders. Also, certain states require any communication letters prepared by the auditor to be submitted with the annual filing. If the organization changes auditors, a potential subsequent auditor may ask to see the communication letters, as well.

Who Really Owns a Nonprofit?

I nice article by The Foundation Group

The concept of who owns a nonprofit organization can be hard for some to grasp, especially given that the answer is, “No one…and everyone!” We encounter this confusion with new clients on a fairly regular basis. And, given people’s understanding of how basic business operates, it is understandable. In order to fully appreciate the concept of “non-ownership”, it is helpful to first talk about the various types of business entities. Then, we’ll look at organizational purpose. By the end of the article, it should make a lot more sense....See full article here..

NONPROFIT YEAR-END FINANCIAL STATEMENT AUDIT (OR REVIEW) PROCESS IN A NUTSHELL (PART 2 of 5)

THE YEAR-END FINANCIAL STATEMENT PROCESS:

A Practical Guide for Small Nonprofit Organizations having a CPA Audit (or Review)

(Part 2 of 5)

Part II: DIFFERENT ROLES IN THE AUDIT PROCESS

A. Governance’s Role in the Audit Process (The Board):

Unlike a small business, a nonprofit organization does not have “owners”. A nonprofit is “governed” by a board of directors under the direction of the organization’s bylaws and state law. The Attorney General (or other state official) provides oversight and regulates all the charities operating in the state. Additionally, because of its tax exempt status, the organization must adhere to IRS regulations as well. The board acts as trustee of the organization's assets and ensures that the nonprofit is well managed, fiscally sound and adhering to its mission and exempt purpose. In doing so, the board must exercise proper oversight of the organization's operations and maintain the legal and ethical accountability of its staff and volunteers. Generally, board members are legally responsible and have the ultimate authority over the organization. All board members should be familiar with the organization’s bylaws, finances, annual audit and Form 990. The executive director may manage the day to day operations, but major decisions should have direct board approval. It is also important that matters involving the executive director’s compensation be decided by the board. All audits will involve governance (the board). In the absence of an audit committee, the independent board members (i.e., unpaid) will perform the audit oversight function. This involves the following basic duties: (1) Overseeing the accounting and financial reporting processes of the organization and the audit of its financial statements; (2) Annually retaining or renewing the retention of an independent auditor; and (3) Reviewing with the independent auditor the results of the audit (including the management letter). All board matters should be documented in proper meeting minutes. The organization is required to have a Conflict of Interest policy to show how it makes decisions involving interested (i.e., related) parties.

B. Management’s Role in the audit process: (Executive Director)

In many organizations, the board hires an executive director to manage the operations. The position usually reports to the executive committee or directly to the full board of directors. In most cases, a paid executive director is not a voting member of the board but the bylaws of an organization may dictate otherwise. Although not on the audit committee, the executive director will usually be the point person and work with the auditor during the audit process.

C. The Independent Accountant’s Role in the Audit Process (CPA)

In a financial statement audit, the CPA expects the organization’s management to present the financial statement figures at year end. Furthermore the auditors will want explanations and evidence to support the figures.

Audits and Reviews are attest engagements that require independence. Services performed in conjunction with Audits or Reviews are called non-attest services. Specific rules have to be followed regarding non-attest services in order for the CPA to remain independent. Some non-attest services that frequently are performed in conjunction with an audit (or review) engagement are financial statement preparation, accounting adjustments, reconciliations, functional expense allocation assistance and tax preparation. Original bookkeeping or major overhauls of financial data cannot be performed in an attest engagement. Importantly, the auditor cannot participate in the decision making process of the client. Audit standards also dictate that if the auditor assists too significantly in the financial statement preparation process, independence could be deemed to be impaired. In order to remain independent while performing these non-attest services, special precautions have to be followed. The organization’s management has to be responsible for the non-attest service by doing the following (1) designating an individual who possesses suitable skills to oversee the service; (2) evaluate the adequacy and results of the services performed; and (3) accept responsibility for the results. Under no circumstances can the CPA assume management responsibilities in an attest engagement. Some organizations hire an accountant or qualified bookkeeper to perform year-end close services before an audit or review engagement begins.

Auditing standards also require certain “disclosures” to be made by the organization. These come in the form of footnotes that follow the financial statements. The CPA’s assistance in preparing the footnotes disclosures is another type of non-attest service. The auditor will need to obtain information and evidence to support the financial statement disclosures. Common areas requiring disclosures are Accounting Policies, Fixed Assets, Notes Payable, Leases, Related Parties, Contingencies, Retirement Plans, Restricted Net Assets, Pledges / Contributions, Joint Costs and Subsequent Events.

The following language is part of the standard engagement letter which outlines the auditor’s role:

Audit procedures will include tests of documentary evidence supporting the transactions recorded in the accounts, tests of the physical existence of assets, and direct confirmation of receivables and certain assets and liabilities by correspondence with selected individuals, funding sources, creditors, and financial institutions…. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements….An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements…..Our audit will include obtaining an understanding of the Organization and its environment, including internal control, sufficient to assess the risks of material misstatement of the financial statements and to design the nature, timing, and extent of further audit procedures.